MyCIF P2P Financing: How Malaysian MSMEs Can Access More Growth Capital

For many Malaysian micro, small and medium enterprises, securing sufficient financing can be one of the biggest barriers to growth.

A business may have confirmed orders, recurring customers and strong commercial potential, yet still struggle to obtain the working capital required to purchase inventory, fulfil contracts, invest in equipment or bridge payment cycles.

Peer-to-peer financing offers an alternative route by connecting eligible businesses directly with private investors through platforms registered with the Securities Commission Malaysia. Through the Malaysia Co-Investment Fund, or MyCIF, qualifying issuers may receive additional co-investment alongside the money raised from private investors.

This public-private financing model can help eligible Malaysian MSMEs raise a larger amount of funding while benefiting from the reach, efficiency and flexibility of a regulated P2P financing platform.

What Is the Malaysia Co-Investment Fund?

MyCIF was established by the Government of Malaysia under Budget 2019 and is administered by the Securities Commission Malaysia. Its purpose is to support Malaysian MSMEs by co-investing alongside private investors through participating equity crowdfunding and peer-to-peer financing platforms.

Rather than replacing private-sector investment, MyCIF is designed to strengthen it.

A business must first attract financing from private investors through a participating P2P platform. Subject to eligibility, available allocation and approval, MyCIF may then contribute additional capital to the campaign according to the applicable co-investment ratio.

This structure combines:

- Private investor participation;

- Due diligence and credit assessment by the P2P platform;

- Government-supported co-investment; and

- A regulated digital fundraising process.

The Securities Commission has described participating P2P platforms as professional gatekeepers that conduct due diligence before campaigns are offered to investors. Private investors subsequently assess the financing opportunity and decide whether to provide capital.

How Does MyCIF Co-Investment Work for P2P Issuers?

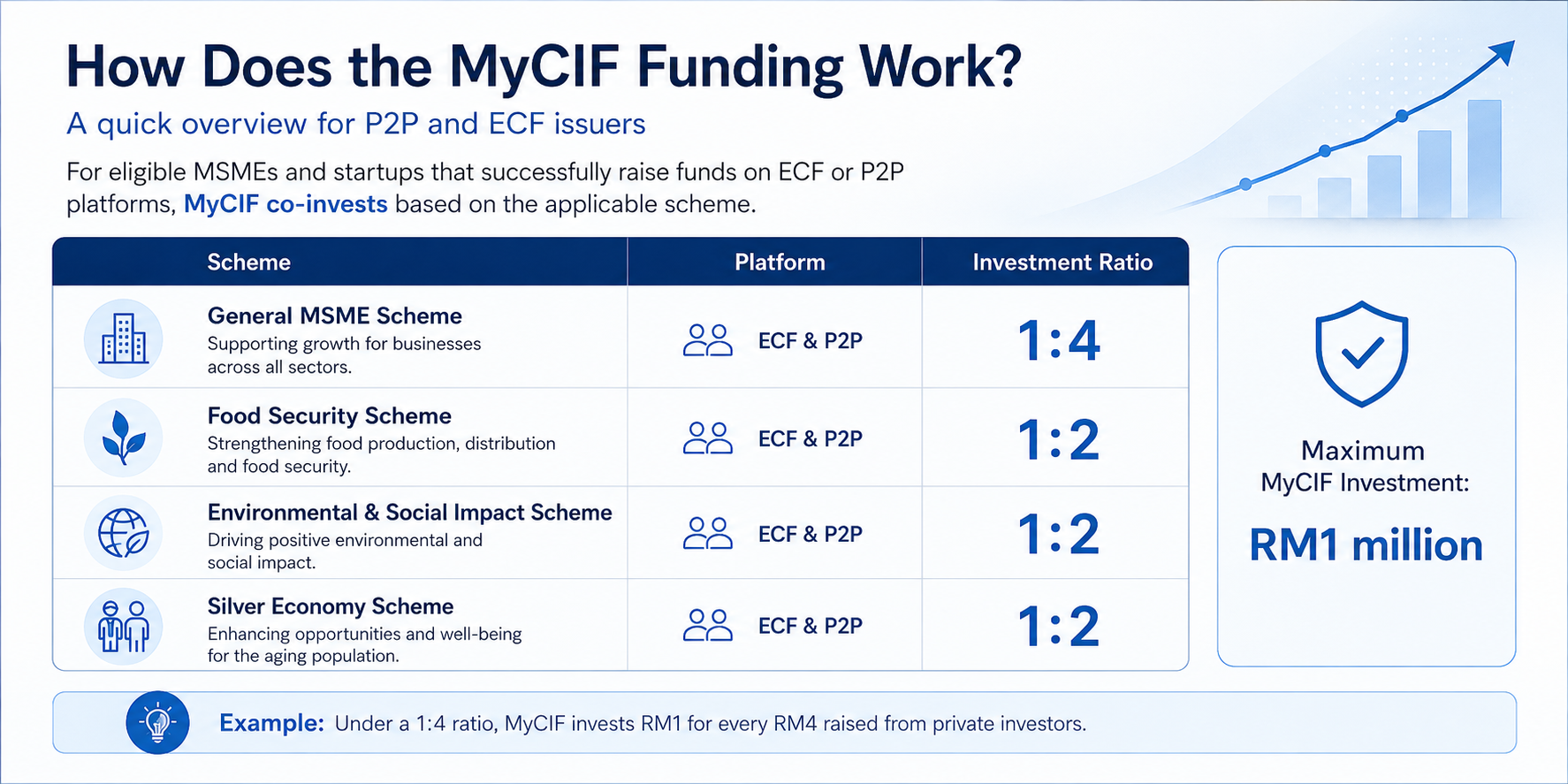

Under the General MSME Scheme, MyCIF may co-invest on a 1:4 basis.

This means that MyCIF may invest RM1 for every RM4 successfully raised from private investors through a participating P2P platform. The maximum MyCIF investment is generally limited to RM1 million for each qualifying P2P campaign.

Example: General MyCIF P2P campaign

Suppose an eligible SME wishes to raise RM1 million.

Under a 1:4 co-investment structure, the financing could potentially comprise:

| Source of financing | Amount |

|---|---|

| Private P2P investors | RM800,000 |

| MyCIF co-investment | RM200,000 |

| Total financing raised | RM1,000,000 |

The MyCIF contribution does not eliminate the need to attract private investors. Instead, it supplements private capital once the relevant requirements have been fulfilled.

Why MyCIF Can Be Valuable to P2P Issuers

1. Access to a broader pool of financing

The most direct advantage is the opportunity to combine private investor capital with MyCIF co-investment.

For a qualifying General Scheme campaign, every RM4 raised from private investors may attract an additional RM1 from MyCIF. This can help an issuer reach a larger overall financing amount without relying solely on private capital.

For an SME, the additional funds could support:

- Working capital requirements;

- Inventory purchases;

- Contract or project execution;

- Supplier payments;

- Equipment acquisition;

- Business expansion;

- Payroll and operating expenses;

- Short-term cash-flow gaps; or

- Other approved business purposes.

2. Potentially stronger campaign momentum

MyCIF participation can provide an additional source of capital alongside private investors.

While it does not guarantee that a campaign will be fully funded, the co-investment structure may make it easier for an eligible issuer to assemble the total financing required once sufficient private investor support has been secured.

It also allows private capital to have a greater cumulative effect. Under a 1:4 structure, RM800,000 raised privately could potentially support a RM1 million campaign after the corresponding MyCIF contribution.

3. Financing outside conventional bank lending

P2P financing can provide an additional option for businesses that:

- Require faster working-capital solutions;

- Have reached their internal bank borrowing limits;

- Need financing matched to a particular contract or cash-flow cycle;

- Have limited fixed assets available as collateral;

- Want to diversify their financing sources; or

- Prefer a digitally administered application process.

P2P financing is not automatically easier than bank financing. Issuers remain subject to due diligence, credit assessment, documentation requirements and investor demand. However, the assessment may place greater emphasis on the business, its financial position, transaction history, repayment capacity and financing purpose rather than relying exclusively on traditional collateral.

4. Preferential co-investment for selected strategic sectors

Certain eligible businesses may qualify for MyCIF’s targeted schemes, which currently include preferential 1:2 co-investment ratios.

Under a 1:2 ratio, MyCIF may invest RM1 for every RM2 successfully raised from private investors. The MyCIF website identifies targeted schemes for food security, environmental and social impact, and the silver economy.

Example: 1:2 strategic co-investment

For a qualifying RM900,000 campaign:

| Source of financing | Amount |

|---|---|

| Private P2P investors | RM600,000 |

| MyCIF co-investment | RM300,000 |

| Total financing raised | RM900,000 |

Compared with the General Scheme, a qualifying strategic campaign may therefore receive a larger MyCIF contribution relative to the amount raised privately.

Admission to a strategic scheme is not automatic. The participating P2P platform must submit the relevant application on behalf of the issuer, and the campaign must fulfil the specific criteria determined by the Securities Commission.

MyCIF Food Security Scheme

The Food Security Scheme supports eligible MSMEs operating in the upstream segments of:

- Agriculture;

- Agritech;

- Bio-economy; and

- Related food-security activities.

Eligible P2P campaigns may receive MyCIF investment at a 1:2 ratio. The official MyCIF information also identifies a potential 0% financing-rate incentive on the MyCIF-funded portion for qualifying P2P campaigns under this scheme.

This may be especially relevant to businesses involved in areas such as farming technology, agricultural production, sustainable inputs, food-production systems and other qualifying upstream activities.

Environmental and Social Impact Scheme

The Environmental and Social Impact Scheme supports eligible MSMEs creating measurable impact in designated areas such as:

- Community development;

- Education;

- Environmental protection;

- Food security; and

- Healthcare.

Qualifying campaigns may benefit from the preferential 1:2 MyCIF co-investment ratio. Businesses must also meet the requirements under the applicable MyCIF Impact Investment Framework.

Issuers applying under this scheme should be prepared to explain clearly:

- The social or environmental problem being addressed;

- The activities financed through the P2P campaign;

- The beneficiaries of the project;

- The intended measurable outcomes; and

- How impact data will be collected and reported.

Participating platforms are required to procure annual impact reports from issuers funded under the scheme for consolidated reporting to the Securities Commission.

Silver Economy Scheme

The Silver Economy Scheme supports eligible MSMEs providing services or innovative solutions for Malaysia’s ageing society and care economy.

Relevant focus areas include:

- Healthcare services;

- Disability-support services;

- Health technology and innovation;

- Aged-care services; and

- Childcare services.

Eligible P2P campaigns may qualify for a 1:2 co-investment ratio, subject to the scheme’s requirements and approval.

This creates financing opportunities for businesses developing practical solutions for demographic and care-related needs, including care providers, specialised health-service companies and technology-enabled care platforms.

Islamic Risk-Sharing Incentives

MyCIF has also introduced incentives to promote Islamic risk-sharing financing structures based on concepts such as Musharakah and Mudharabah.

For eligible P2P campaigns structured under approved Islamic risk-sharing models, the current programme provides for:

- MyCIF participation on a first-loss basis; and

- An additional MyCIF investment at a 0% financing rate.

These incentives are stated to be available until the end of 2026, subject to the applicable conditions, allocation and regulatory approval.

Businesses interested in these structures should engage with a participating P2P platform early, as the proposed financing arrangement must be structured in accordance with the relevant Shariah and MyCIF requirements.

Who Is Eligible for MyCIF P2P Co-Investment?

Under the MyCIF terms and conditions amended on 21 November 2025, a P2P issuer must satisfy three principal requirements:

- It must be a permitted issuer under the Securities Commission’s Guidelines on Recognized Markets.

- It must fall within SME Corporation Malaysia’s definition of a micro, small or medium enterprise.

- It must meet the financing and credit requirements imposed by the participating MyCIF P2P platform.

Meeting these basic criteria does not create an automatic entitlement to funding.

The issuer must still pass the platform’s due-diligence and credit-assessment process, successfully raise the required private-investor portion and, where applicable, obtain admission to the relevant strategic scheme.

The Securities Commission retains discretion to refuse MyCIF investment in a campaign, and co-investment is subject to available funds.

What Documents Should a P2P Issuer Prepare?

A well-prepared application can improve the efficiency of the assessment process. Depending on the business and proposed financing structure, the P2P platform may request:

- Company registration and corporate documents;

- Directors’ and shareholders’ information;

- Audited financial statements;

- Latest management accounts;

- Recent business bank statements;

- Credit-report consent forms;

- Existing borrowing and repayment schedules;

- Accounts receivable and payable ageing;

- Sales records and major customer information;

- Contracts, purchase orders or invoices;

- Details of the intended use of funds;

- Cash-flow projections;

- Information on related companies; and

- Personal or corporate guarantees where required.

Businesses seeking admission to a strategic scheme may need additional evidence demonstrating that their activities fall within the relevant sector and satisfy the programme’s specific conditions.

For example, an environmental or social-impact applicant may need to submit impact objectives, performance indicators and an annual reporting plan.

How to Apply for MyCIF Through a P2P Platform

The application process generally follows three stages.

Step 1: Apply through a participating P2P platform

The issuer submits its financing application and supporting documents to a P2P operator participating in MyCIF.

The platform evaluates the company’s financial condition, repayment capacity, credit profile, management, financing purpose and overall risk.

Step 2: Raise financing from private investors

Once approved and hosted, the financing campaign is offered to private investors through the platform.

Investors decide whether to participate based on the campaign information, risk assessment, financing terms and expected return.

Step 3: Access MyCIF co-investment

After the applicable private-funding requirement has been fulfilled, the participating platform facilitates the MyCIF process for an eligible campaign.

The Securities Commission’s official application summary similarly describes the process as applying through a participating platform, obtaining private funding and then accessing MyCIF assistance through the platform where eligible.

Issuers generally do not approach MyCIF independently for an ordinary campaign. The participating P2P platform manages the relevant submission and allocation process.

Is MyCIF Funding Guaranteed?

No.

MyCIF is a co-investment programme, not an automatic grant or guaranteed financing facility.

Several conditions remain important:

- The issuer must meet the qualifying criteria.

- The P2P platform must approve the financing application.

- The campaign must obtain the necessary support from private investors.

- Strategic-scheme applications must be approved.

- MyCIF funds must remain available.

- The campaign must comply with all relevant terms and conditions.

- The Securities Commission retains discretion over MyCIF investments.

MyCIF co-investments are provided on a first-come, first-served basis, and further investment may be halted once the available allocation has been reached.

Businesses should therefore apply early and provide complete, accurate documentation to minimise avoidable delays.

Can MyCIF Reduce the Issuer’s Financing Cost?

The General Scheme does not necessarily mean that the issuer receives grant funding or interest-free financing. The applicable pricing and repayment obligations depend on the terms of the P2P campaign.

However, selected strategic schemes may offer additional incentives. In particular, the official MyCIF materials describe a 0% financing-rate incentive for the MyCIF-funded portion of qualifying P2P campaigns under the Food Security Scheme and Islamic risk-sharing incentives.

The actual blended financing cost will depend on:

- The amount contributed by private investors;

- The MyCIF contribution;

- The applicable investor return or financing rate;

- Platform and administrative fees;

- The financing tenure;

- The repayment structure; and

- Any special scheme incentives.

Issuers should request a complete financing illustration from the P2P platform before accepting an offer.

How to Improve the Chances of a Successful MyCIF-Supported Campaign

Present a clear and credible use of funds

Businesses should state precisely how the financing will be used.

“Working capital” alone may be too broad. A stronger explanation would identify the amount required for inventory, supplier payments, contract mobilisation, equipment or other specific expenditure and show how the financing will generate sufficient cash flow for repayment.

Demonstrate repayment capacity

P2P financing remains repayable financing.

Issuers should provide evidence that anticipated operating cash flows are sufficient to service the financing. Useful supporting information may include historical bank transactions, confirmed contracts, recurring sales, customer payment records and reasonable cash-flow projections.

Maintain clean and complete financial records

Unexplained bank transactions, inconsistent management accounts, undisclosed borrowings or incomplete corporate information can delay an assessment and reduce investor confidence.

Management accounts should reconcile, as far as reasonably possible, with bank statements, tax records and audited financial information.

Address credit issues transparently

An existing late payment, legal case or adverse credit record does not always lead automatically to rejection. However, failure to disclose material information can seriously damage credibility.

Issuers should explain the cause, current status and corrective action for any adverse item.

Apply for the correct MyCIF scheme

Businesses operating in food security, agriculture, healthcare, education, environmental impact, community development or the care economy should identify their potential eligibility at the beginning of the application.

A well-supported strategic-scheme application may qualify for a more favourable 1:2 co-investment ratio, but the business must demonstrate genuine alignment with the scheme rather than merely adopting broad impact language.

MyCIF’s Contribution to Malaysia’s MSME Financing Market

MyCIF has become a significant part of Malaysia’s alternative-financing ecosystem.

According to the Securities Commission, by the end of 2024 MyCIF had recorded approximately RM1.19 billion in total co-investments, with more than 9,500 MSMEs benefiting. The SC also reported that each ringgit co-invested by MyCIF attracted approximately 4.1 times as much private-sector funding.

The figures displayed on the MyCIF microsite for the period from the fourth quarter of 2019 to the fourth quarter of 2025 indicate:

- 11,512 MSMEs had received co-investment;

- Approximately RM1.50 billion had been co-invested;

- Approximately RM6.21 billion had been invested privately alongside MyCIF; and

- 89% of MyCIF co-investments benefited micro and small enterprises.

These results demonstrate how public co-investment can mobilise substantially more private capital for Malaysian businesses.

Raise P2P Financing Through a Participating MyCIF Platform

For an eligible Malaysian MSME, MyCIF can make P2P financing a more powerful source of business capital.

Through the General Scheme, MyCIF may contribute RM1 for every RM4 raised privately. Businesses in qualifying strategic sectors may potentially access a more favourable 1:2 co-investment ratio and, in selected cases, additional financing incentives.

FBM Crowdtech Sdn. Bhd., which operates the Alixco platform, is listed by the Securities Commission as a participating MyCIF P2P financing platform.

Businesses considering P2P financing can submit their financial and corporate information for an initial assessment. Where the issuer and campaign qualify, the participating platform can evaluate the appropriate financing structure and facilitate the relevant MyCIF application.

Frequently Asked Questions

What does MyCIF mean?

MyCIF stands for the Malaysia Co-Investment Fund. It is a government-established fund administered by the Securities Commission Malaysia that co-invests alongside private investors through participating ECF and P2P platforms.

How much will MyCIF invest in a P2P campaign?

Under the General Scheme, MyCIF may invest RM1 for every RM4 successfully raised from private investors. The maximum MyCIF investment is generally RM1 million per qualifying P2P campaign.

Which schemes offer a 1:2 co-investment ratio?

The current MyCIF microsite identifies the Food Security Scheme, Environmental and Social Impact Scheme and Silver Economy Scheme as offering a 1:2 ratio for qualifying campaigns.

Does an SME apply directly to MyCIF?

Ordinarily, the SME applies for financing through a participating P2P platform. The platform conducts its assessment and facilitates the MyCIF submission for eligible campaigns.

Is MyCIF a grant?

MyCIF co-investment in a P2P campaign is generally part of the financing raised by the issuer and should not be treated as a business grant. The issuer remains responsible for complying with the campaign’s financing and repayment terms.

Can every Malaysian SME obtain MyCIF financing?

No. The business must be a permitted P2P issuer, qualify as an MSME, satisfy the platform’s requirements and successfully attract the required private investment. MyCIF participation also remains subject to available allocation and the Securities Commission’s discretion.

Can an existing P2P borrower apply?

Potentially, but approval will depend on the issuer’s existing exposure, repayment record, current financial position, total debt obligations and capacity to service additional financing.

When should a business apply?

Businesses should apply before the capital becomes urgently overdue. A timely application allows the platform to review the documents, clarify financial information, structure the campaign and consider whether the issuer qualifies for a strategic MyCIF scheme.

Important notice

MyCIF eligibility and co-investment are not guaranteed. All applications remain subject to the participating platform’s assessment, investor demand, available MyCIF allocation, the applicable MyCIF terms and conditions, and the Securities Commission Malaysia’s approval and discretion. Programme terms may be amended. Issuers should refer to the latest official MyCIF information and obtain a complete financing illustration before proceeding.

Important Disclaimer: T&C apply. Investments in P2P and ECF campaigns may lead to the loss of the entire capital invested. Do not invest more than you can afford to lose. This is not an offer or solicitation to make any type of investments. This article has not been reviewed by the Securities Commission Malaysia.